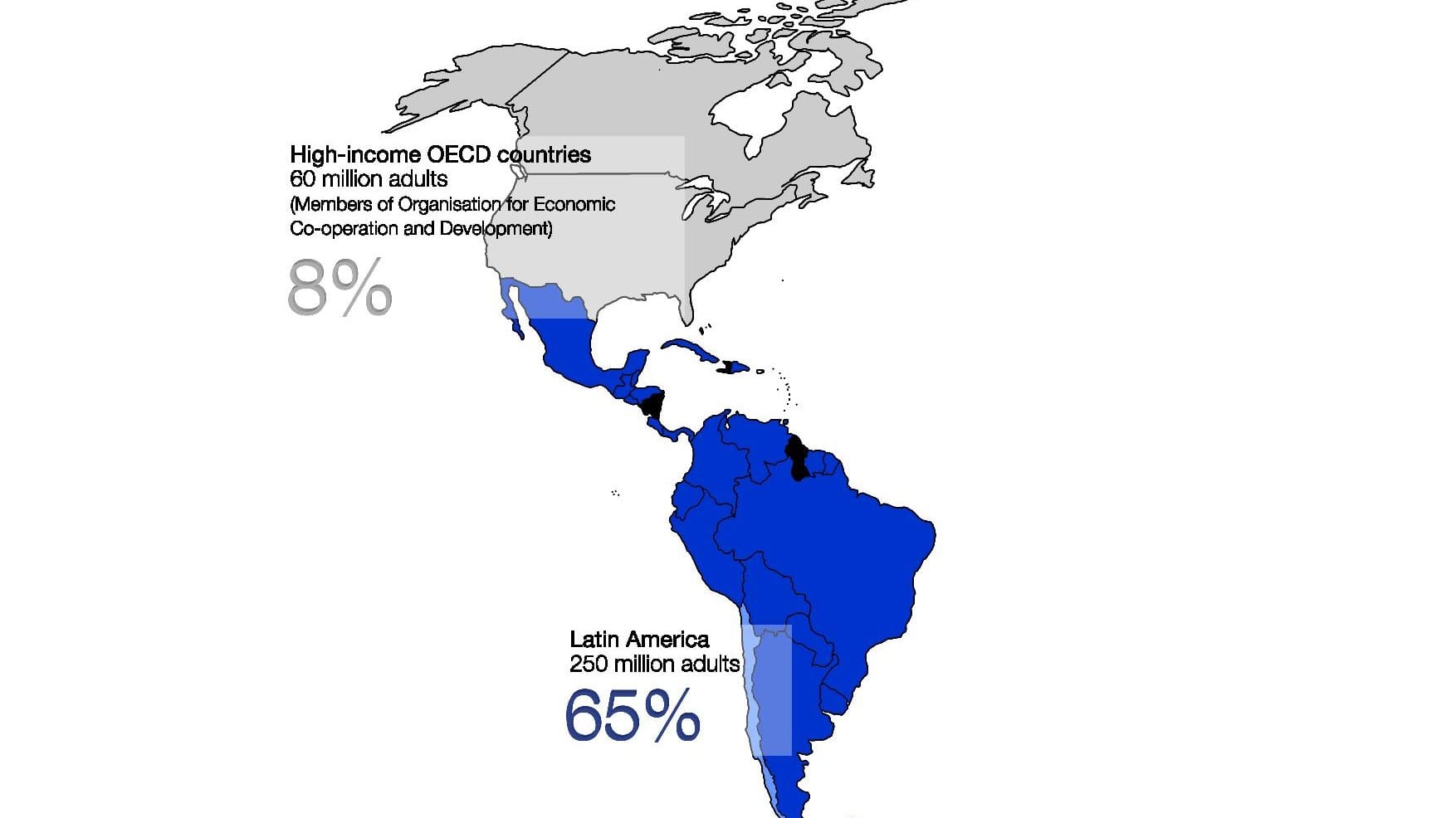

Did you know that just over 2.5 billion of the world’s adults don’t use banks? Did you also know that every day, 25,000 children die due to poverty-related issues? It would be reasonable to assume that microcredit, or small loans, typically of a few hundred dollars each, would be akin to a drop in an ocean. But surprisingly, this drop has turned into a tidal wave.

The microcredit movement broke into the mainstream consciousness in 2006 when Grameen Bank founder, Muhammad Yunus, won the Nobel Peace Prize. His bank had broken new ground in the market of microcredit back in 1976 and 30 years later he was celebrated for his achievements. The idea was simple: Grameen would lend an average of 400 USD per person to those with no access to other credit facilities, thereby creating opportunities for self-employment and self-enrichment.

Unlike other banks, whose main objective is to make a profit, the Grameen Bank aims to alleviate poverty by servicing the poor. Operating mainly in rural Bangladesh, the Grameen Bank lends mostly to women, in an effort to raise their status, and also believing that they are better credit risks. The results were astounding: repayment rates were better than most commercial banks at an unprecedented 98 per cent.

The Grameen Bank's operations would horrify conventional, conservative bankers. There are no contracts between the bank and the borrower. No collateral is needed for a loan. If a borrower is unable to pay, they won’t be taken to court. Instead, the bank works harder to help the borrower overcome their obstacles so they can make a profit and thereby repay the loan. Furthermore, conventional banks view the poor as high credit risks so they charge extremely high interest rates for a loan. The Grameen Bank, on the other hand, charges only 11 per cent, which is lower than the Bangladeshi government rate. It also has a policy that the interest should under no circumstance be higher than the amount of the original loan. Interest paid on deposits is extremely generous, with a minimum rate of 8.5 per cent.

To date, the Grameen Bank has lent out 8.5 billion USD, helping eight million of Bangladesh's poor. It’s a great example of what can be done to alleviate poverty. Unfortunately, recent statistics show that only around 150 million of the world’s 2.5 billion unbanked are currently being served by such facilities. For real change to take affect, benefactors and banks need to wake up to the fact that microcredit works.